Alexander Hamilton began the tradition of big government conservatism. His followers have included Henry Clay, Abraham Lincoln, Theodore Roosevelt, Nelson Rockefeller and George W. Bush. In today's nomenclature, Hamilton was the first "Republican". In other words, the Republicans have been traditionally the party of inflation, and it was only intermittently, during the century from 1871 to 1971, that the Republicans could claim to support hard money. For the first 25 years of that century, the Democrats too were a hard money party. It was only by default that the Republicans became associated with monetary stability in 1896, and they have always been wobbly supporters. The Benjamin Strong Fed was inflationary, with the approval of the Harding and Coolidge administrations. The deflation of the Hoover administration was a product of Fed policy and had little to do with Hoover. Yet, the segment of Americans who are able to grasp this issue and are anti-inflation mostly remain within the Republican party. perhaps the greatest political betrayal of the late twentieth century was Ronald Reagan's decision to adopt Keynesian (supply side) deficit and expansionist policies despite his mandate from the Reagan Democrats. Both American political parties today descend from Hamiltonian centralizing, banking and rationalizing theories. Those who are skeptical of central economic planning, big government, Keynesian economics and the ability of academics to foresee progress have nowhere to turn. Both parties are marionettes of Wall Street.

Hamilton argued for federalism and centralization of government, a central bank and for banking in general. He was an elitist who believed in the ability of bankers and merchants to make use of artificially created money in the form of bank notes to expand the economy, and this theory provided the fulcrum on which his advocacy of the Bank of the United States pivoted. He argued that bankers can rationally assess risk. He makes the same aarguments that we hear on CNN and read in the New York Times today. The themes that Hamilton emphasized, paper money, central banking, rationality of business strategy, the importance of fractional reserve banking to stimulating the economy and the ability of the business elite to build the economy were paradigms for subsequent Whig, progressive, and New Deal ideologies, of which George W. Bush and Barack Obama are the latest manifestations.

There were two strange turns in the history of the elitist, centralizing ideology. At first, Jefferson and then Jackson reacted to the Federalist-Whig philosophy of Hamilton, Clay (and then Lincoln) by advocating decentralization and hard money. Thus, decentralization and hard money were benign views that represented the values of the workman. The loco focos and workingmen's parties of the 1820s and 1830s reflected the Jacksonian resentment of banks, business monopolies, internal improvements (the profits from which went into the pockets of elite Whig stockholders) and the central bank.

In the Gilded Age, the

laissez-faire ideology became associated with the elite. This was a reversal. It occurred because

laissez-faire became associated with social Darwinism in the ideas of Spencer and William Graham Sumner. Thus, the Mugwump Republicans carried forward the Republican centralizing and elitist views but adopted the laissez-faire and hard money philosophy of Jefferson and Jackson because it fit the ideas of social Darwinism. This deprived the hard money position of its benign, pro-worker foundation. So by adopting laissez-faire the Republicans weakened the force of its claims and destroyed it. They did this by claiming that only the fittest would benefit from hard money. This opened the door for the Democrats to claim that central banking, the chief elitist tool, was Democratic. Then, Progressivism removed the laissez-faire element from the Gilded Age's rationalizing philosophy, retaining the traditional Hamiltonian claims of rationality of business and banking elites, the importance of a centralized state, the virtue of elite experts, and centralized banking.

In 1790 Hamilton, as the first Secretary of the Treasury, wrote his

Report on Public Credit and

Second Report for Further Provision Necessary for Establishing Public Credit. He also wrote a report on the

Constitutionality of the Bank and

Report on Manufactures. The issues in the

Report on Public Credit directly concerned the question of centralization and of establishing a central bank. The questions that faced the nation at that point concerned federal assumption of the states' revolutionary war debts and how such assumption would be arranged; and the question of whether the federal government should honor its debts at par, especially because speculators had purchased bonds at steep discounts; and the payment of interest on the outstanding debt. Hamilton argued for stabilizing the nation's credit record and honoring debts.

Hamilton argues for the importance of federal debt to the expansion of the US economy. He argues that a funded debt (which has been converted into bonds and for which there is funding) can expand economic activity because the debt can function as money and because debt will cause real estate prices to appreciate. The notion that inflation can help real estate investors finds legitimacy in Hamilton's report to the first Congress. He writes (p. 6):

"The effect, which the funding of the public debt, on right principles, would have upon landed property, is one of the circumstances attending such an arrangement, which has been least adverted to, though it deserves the most particular attention. The present depreciated state of that species of property is a serious calamity. the value of cultivated lands, in most of the states, has fallen since the revolution from 25 to 50 per cent. In those farthest south the decrease is still more considerable...This decrease in the value of lands, ought, in a great measure, to be attributed to the scarcity of money."

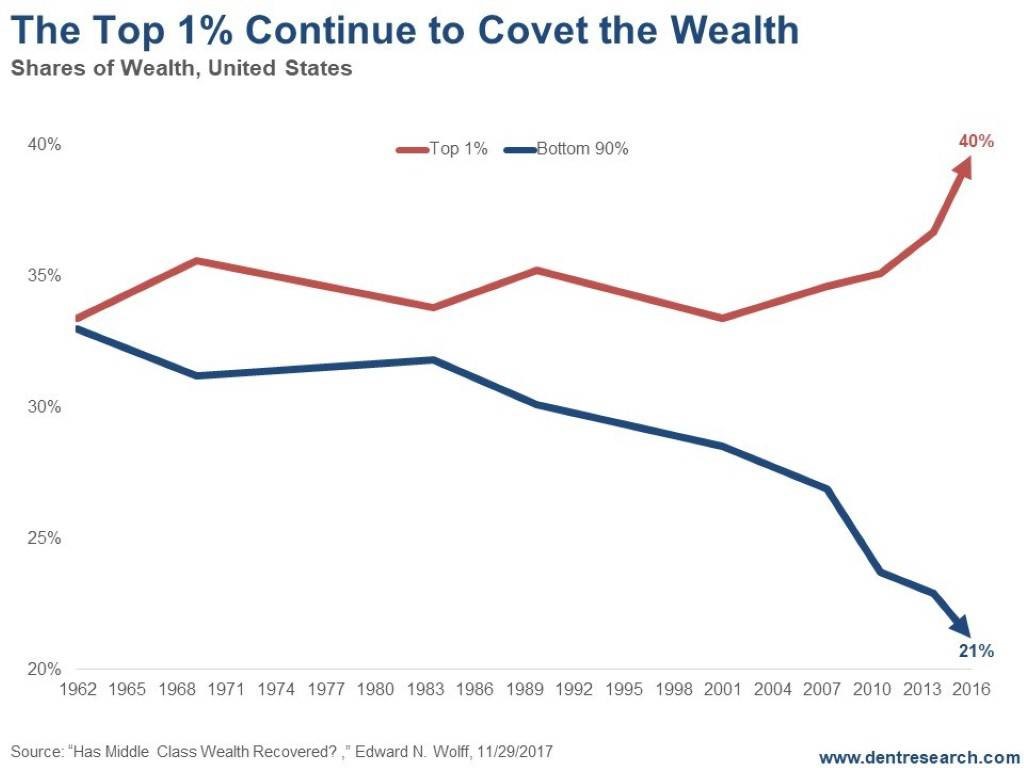

Thus, Hamilton was among the first Americans to recognize the possibility of monetary expansion to transfer wealth to the landed, the stock holder and the wealthy. This theme was to continue throughout American history except for the four post Civil War decades because of the ideology of social Darwinism. Notably, it was in the post Civil War period that the United States made the lion's share of its economic progress, beginning with the abolition of the bank in 1836 through the advent of Progressivism in 1905.

Hamilton's preference for centralization is explicit in

Report on Public Credit. It is much better, he argues, for creditors to receive payments from one source than from the several states. If the central government takes responsibility "there can be no competition for resources" and "different states, from local considerations, would in some instances have recourse to different objects, in others to the same objects, in different degrees, for procuring the funds of which they stood in need. It is easy to conceive how this diversity would affect the aggregate revenue of the country....hence the public revenue would not derive the full benefit of those articles from state regulation." Moreover, "if all the public creditors receive their dues from one source, distributed with an equal hand, their interest will be the same. And having the same interests, they will unite in support of the fiscal arrangements of the government; As these, too, can be made with more convenience, where there is no competition: These circumstances combined will insure to the revenue law a more ready and more satisfactory execution."

It was important to Hamilton to establish the national credit and he was certainly concerned with the interests of creditors, whom he saw as furthering national goals. To this end, Hamilton emphasized the importance of repaying the national debt, including interest. In the end there was a slight reduction in interest (see Elkins and McKitrick,

The Age of Federalism.) But the nation did not make good on the currency it used to pay for the Revolutionary War, the Continentals. The federal government allowed them to become worthless.

In

Second Report on the Further Necessity for Establishing Public Credit, Hamilton argues for a central bank and extols fractional reserve banking. Little has been added since Hamilton.

One passage that caught my eye might be extended to the subprime crisis and every other boom and bust bubble that has occurred since, including the one that occurred in 1790 in New York with respect to speculation in the stock of the First Bank of the United States:

"It may be said that as Bank paper affords a substitute for specie, it serves to counteract that rigorous necessity for the metals...and...it would retard those oeconomical and parsimonious reforms in the manner of living, which the scarcity of money is calculated to produce...

"There is perhaps some truth...but...of a nature rather to form exceptions to the generality of the conclusion, than to overthrow it...a situation in which a too expensive manner of living of a community compared with its means, can stand in need of a corrective, from distress of necessity, is one which perhaps rarely results, but from extraordinary and adventitious causes, such for example, as a national revolution, which unsettles all the established habits of a people, and inflames the appetite for extravagance, but the illusions of an ideal wealth, engendered by the cause. There is good reason to believe that where the laws are wise and well executed, the oeconomy of a people will, in the general course of things, correspond with its means."

Throughout the two reports on credit, Hamilton emphasizes the rational capacity of bankers and merchants and their sound judgment (e.g., "Those who are most commonly creditors of a nation are, generally speaking, enlightened men...", p. 3,

Report Relative to Public Credit).

Hamilton argues vigorously for the positive effects of monetary expansion and a central bank. He argues that "Gold and Silver, when hey are employed merely as the instruments of exchange and alienation, have been not improperly denominated dead Stock; but when deposited in Banks, to become the basis of a paper circulation...they then acquire life." By depositing money in a bank, merchants enable others to borrow and "It is a well established fact, that Banks in good credit can circulate a far greater sum than the actual quantum of their capital in Gold and Silver. The extent of the possible excess seems indeterminate; though it has been conjecturally stated at the proportions of two and three to one."

This rousing defense of fractional reserve banking presaged two centuries of booms and busts, the most recent being the multi-trillion dollar transfer of wealth to wealthy bankers from the general economy and an aggressive monetary expansion.

Hamilton's ideas were rejected in the early nineteenth century but subsequently adopted by both political parties in the twentieth. Most progress occurred in the 19th. The twentieth century was one of reaction and decline.